IS MY BUSINESS RIGHT FOR FRANCHISING?

One of the most common questions we get from business owners is whether their business is right for franchising. Here […]

IS MY BUSINESS RIGHT FOR FRANCHISING? Read Post »

One of the most common questions we get from business owners is whether their business is right for franchising. Here […]

IS MY BUSINESS RIGHT FOR FRANCHISING? Read Post »

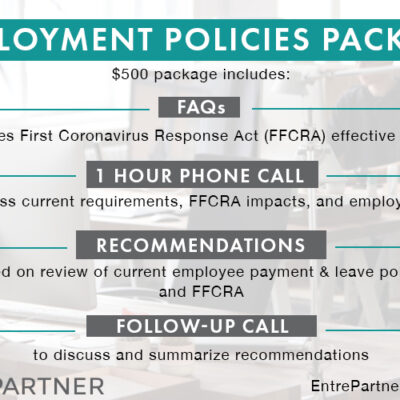

With the effective date of the Families First Coronavirus Response Act (FFCRA) looming, the Department of Labor (DOL) on Saturday,

Both state and federal governments have taken swift action to enact quick and innovative programs to aid small businesses struggling

As entrepreneurs ourselves, we understand the critical value of your time right now and that you want to understand the

WHAT DOES THE CARES ACT MEAN FOR YOUR SMALL BUSINESS? Read Post »

The Families First Coronavirus Response Act (FFCRA) becomes effective on April 2, 2020 and ends December 31, 2020. The FFCRA

The U.S. Small Business Administration (SBA) is offering designated states and territories (including Minnesota) low-interest federal disaster loans for working

INFORMATION ON SBA LOW-INTEREST FEDERAL DISASTER LOANS Read Post »