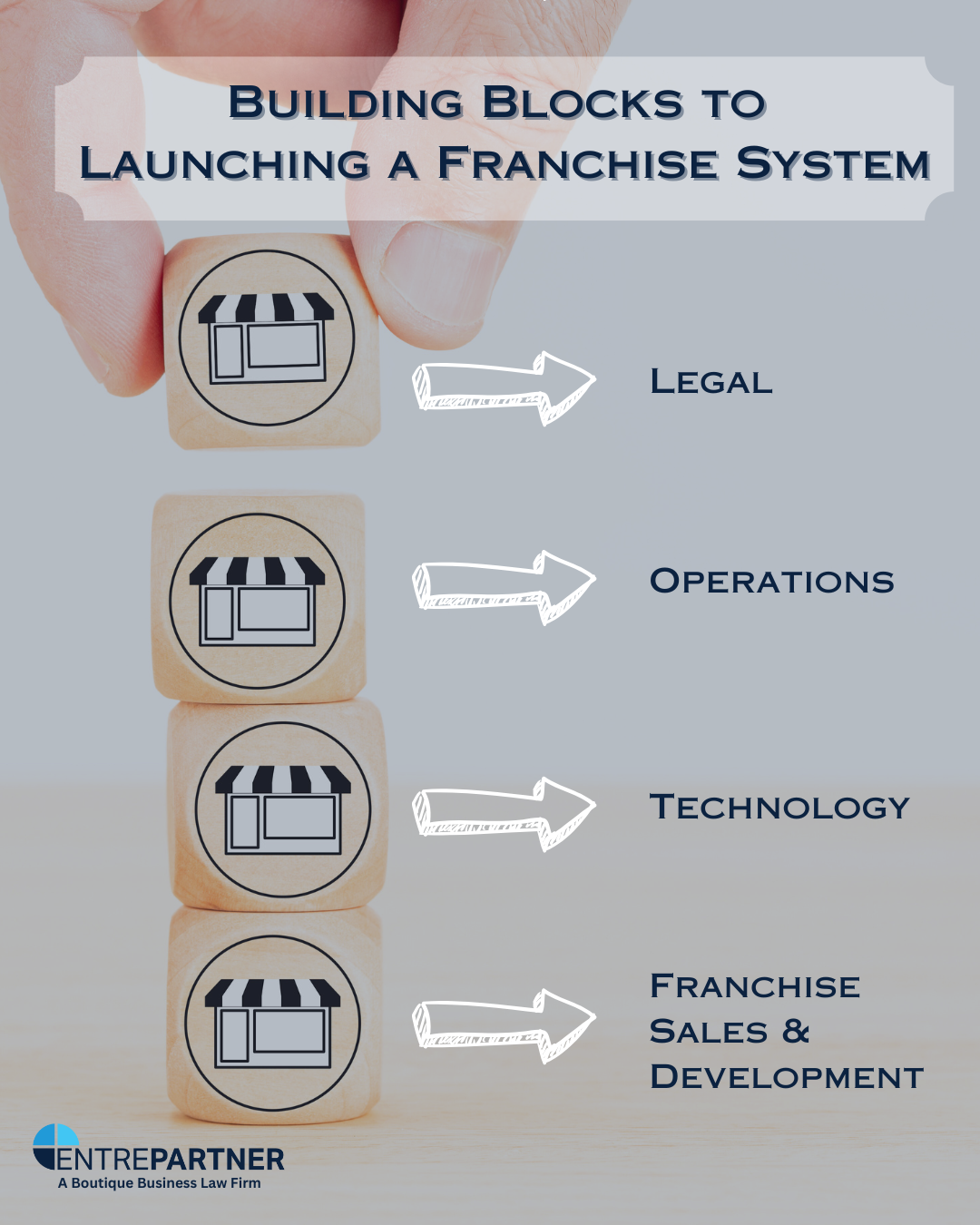

FRANCHISE STARTUP COSTS – WHAT SHOULD YOU REALLY BUDGET FOR?

One of the initial questions potential franchisors inevitably ask us is what sort of budget is needed to establish and […]

FRANCHISE STARTUP COSTS – WHAT SHOULD YOU REALLY BUDGET FOR? Read Post »